The EROI literature suggests EROI needs to be much higher than 1 to sustain economic growth. Also, some estimates of solar panel (PV) EROI are as low as 3. This short article addresses both of these points: https://www.sciencedirect.com/science/article/pii/S254243511...

See [1] for a more in-depth analysis of this, and much more.

"In America, for example, the benchmark measure of inflation (CPI-U) has been modified by ‘substitution’,

‘hedonics’ and ‘geometric weighting’ to the point where reported numbers seem to be at least six percentage

points lower than they would have been under the ‘pre-tinkering’ basis of calculation used until the early 1980s."

Good comment, except I'd point out that plenty of creativity and invention gets employed in the service of rent-seeking: e.g. most of academic economics, and the way it gets used politically.

Check out Michael Hudson and Richard Werner for a dose of reality.

Brexit aside, some well-informed people are advocating a large Sterling devaluation in order to boost competitiveness [1]:

"We should directly address our lack of competitiveness

by the most obvious and effective means available: by

bringing about a substantial devaluation of the currency."

Banks are not merely intermediaries between savers and borrowers. Loans create money, but only loans that are not used to repay other loans result in an increase to the money supply. The following text comes from an ING Bank research note, quoted by The Economist [1]:

"Banks do not view the creation of money as an objective itself. It is a by-product of the banking sector’s business operations. However, it is of great economic and social relevance.

Not every loan ultimately results in new money. The majority of new lending is used to redeem existing loans. Money is only created to the extent the gross lending exceeds the value of the existing loans being redeemed."

That note refers to the "great economic and social relevance" of these banking operations. Here's Professor Richard Werner talking about this at length. [2]

Here's Perry Mehrling (who teaches Coursera's Economics of Money and Banking) weighing in [3]. He explains that it's a nuanced issue but clearly agrees that the "credit creation view" is important and quotes a Group of 30 report:

“In a barter economy, there can rarely be investment without prior saving. However, in a world where a private bank’s liabilities are widely accepted as a medium of exchange, banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet.”

Again banks' role in the creation of M2 money does not reflect how individual retail banks operate.

Just because you have a model that seems to describes the behavior of flock of birds doesn't mean that the model is useful when discussing the anatomy and wing-aerodynamics of individual birds.

You've posted a bunch of links describing the various forms of money and the role of banks in modern (post 18th century) M2 money creation. I know all of this material but it's not relevant to the operations of individual retail banks.

OK, so if each individual retail bank only lends out pre-existing, deposited funds, where does the increase in the money supply come from? Bear in mind that money created as a by-product of bank lending makes up the vast majority of the total money supply in various modern economies (97% in the UK [1]).

The increase occurs because of the different definitions of money. If you define money as the sum of amounts available in demand account at banks (with is roughly what M2 is), then lending from a bank increases this number as the borrowed money ends up in the account of the borrower or in the accounts of the people the borrower spends the money with.

This fact means that retail banks "create money out of nothing" only when money is defined as the sum across all banks of the amounts available to customers on demand. No individual bank "creates money out of nothing", individually they borrow money and lend a fraction of it out; they have balance sheets which balance - i.e. ignoring shareholder equity, for every asset (money owed to them by a borrower), there must be a liability (money they owe to lenders including depositors). The M2 money supply counts the latter but does not deduct the former from the sum; as a result, the M2 money supply has a direct relationship with the total size of retail banking balance sheets.

M2 is an economic statistic and it's behavior tells you nothing about how individual banks operate.

OK, how does that gel with a report from S&P [1] that says:

“Banks lend by simultaneously creating a loan asset and a deposit liability on their balance sheet. That is why it is called credit “creation” – credit is created literally out of thin air (or with the stroke of a keyboard)”?

Also Prof Werner's analysis, he reaches the same conclusion.

That statement is misleading or reflects a misunderstanding on the part of the author.

"Credit" is an accounting concept. Balance sheets are accounting artifacts. The way the bank records it's transactions is a model, not reality. For example, lots of intangibles can have accounting entries created for them for various purposes, but these don't create reality.

Btw, a big problem when discussing bank operations are that the terms "debit" and "credit" can be confusing as their roles are relative to the bank not the customer. Even "asset" and "liability" can be confusing. An Irish media finance and economics professor, Brian Lucey, mixed them up and suggested that a troubled bank could be fixed if it sold its deposits which is impossible - deposits are a liability for banks, not an asset.

Reality is much more simple. Bank lending starts when a customer asks for a loan. Assuming the loan application meets all risk requirements, etc. AND sufficient funds (reserves) are available on the bank's balance sheet, the loan can be issued and the funds transfered to the customer. Reserves are reduced as part of this process but an asset is created for the bank (the loan) so the balance sheet remains the same size.

Well, that's the crux of it right there. You are disagreeing with several authoritative sources who say that no such transfer happens, and in general the loaned funds are created out of thin air.

Standard & Poor's: “Banks lend by simultaneously creating a loan asset and a deposit liability on their balance sheet. That is why it is called credit “creation” – credit is created literally out of thin air (or with the stroke of a keyboard)”

Group of 30: "... banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet."

Richard Werner: "...each individual bank creates credit and money newly when granting a bank loan."

Banks are subject to constraints. They need to retain enough capital to absorb losses on their loan book, and they need to retain enough reserves to cover withdrawals and clearing requirements. They are free to create money "out of thin air" insofar as they meet regulatory requirements associated with those constraints. [1]

You wrote: "I've worked in retail banks and have some hands one (sic) grasp of their day to day operations."

I suggest that your experience does not encompass the whole sector, and that may be the source of your confusion.

Governments aren't striving for ideal outcomes - government is necessarily a bunch of scoundrels whose chief goal is to stay in power, which is achieved by giving sufficient bungs to donors and voters:

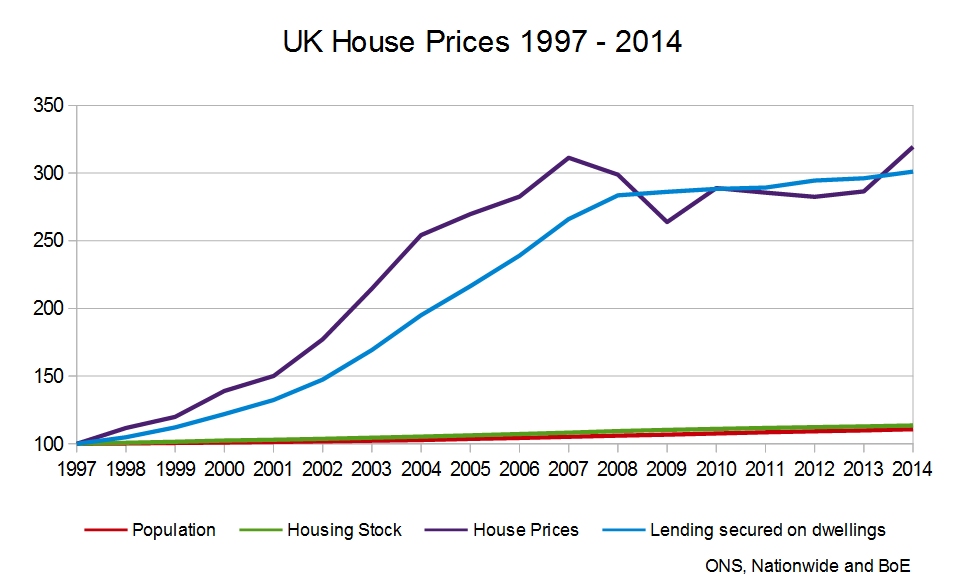

House prices move with mortgage credit growth. Credit growth is one of the key pillars of the politically sustained Ponzi-scheme that is the modern urban housing market.

Banks love mortgages because they are easy, safe ways to earn a bit more than the federal rate.

Wealthy consumers love mortgages because it's a cheap way to leverage a huge asset for market-rate returns.

Normal consumers love mortgages because it allows them to buy a house.

Good luck taking that away.

Additionally, while access to credit raises housing prices, there's no guarantee that removing access to that credit will in any way make housing more affordable for moderate- or low-income people. More people would be forced to rent and it's possible that the wealthy apartment owners will engage in rent seeking and rents will just raise to match or exceed the cost of a mortgage.

That will rob lower income people of their biggest opportunity for wealth creation (housing appreciation) and increase wealth inequality.

But you're ignoring the fact that people are already being priced out of the housing market. The market only continues to gain steam while the next generation can reasonably shoulder the burden being placed on them by the previous. Otherwise those assets are going to deprecate. Credit allowed a handful of people to become incredibly wealthy by becoming rent seekers, while most people didn't realize they had the opportunity. The general consensus seems to be "Tough shit if you weren't born in the 60's - 70's". I don't see that ending well for the economy as a whole.

People will always be priced out of the housing market. Adam Smith observed in the wealth of the nations that once people have the basics housing tends to eat the rest of their income. You can afford to buy/rent closer to where you want to live, or you can afford to buy/rent a bigger place. Since you already have enough for the basics most people find that better housing improves their quality of life.

I have noticed in recent years that improving without changing location or size is also often done as well. A cheap laminate counter is replaced by granite - no change functionally or in size, just an aesthetic change.

Yes. Here in the UK, I have a lot of sympathy with the view that Corbyn's Labour would deliver debt-funded jam today by dumping the burden onto future taxpayers, but the Conservatives have been doing the exact same thing for their own clients, via property inflation.

"Land by its nature is scarce. A site in Mayfair cannot be reproduced like a pair of shoes. The monopoly rent it commands plays no productive role. It acts as a private tax on the productive economy. The question has always been what can be done about it." [1]

I posted that quote because it's the reference I found most speedily to the idea that high land prices impose private (i.e. paid into the private sector) taxation, rather than public. You didn't make the distinction between public vs private taxation in your comment and I thought it should be made.

Public taxation is also involved of course, e.g. when governments need to bail out the banking system; Help to Buy in the UK; etc.

> high land prices impose private (i.e. paid into the private sector) taxation, rather than public

Agreed, though I'm not sure that's much consolation to the ones paying it. With public taxation at least you can hope you're helping to fund something useful.

BTW, you mentioned reservations about possible overspending by Corbyn's Labour. I'm encouraged however by the noises they're making about productivity, e.g. in a recent report:

"The report’s guiding idea is to encourage finance to flow towards productive investment rather than speculation in property. This reflects an old complaint about the City of London: it is a global entrepot with little interest in promoting productive investment in the UK." [1]

And here is a very good primer on the important distinction between productive and unproductive credit. [2]

Mortgages per se aren't the problem; low rates and high LTV are the problem.

I agree that changing this is politically difficult, and it's downright depressing to see discussion threads on the topic filled wall-to-wall with turkeys demanding more Christmas, but there are limits to how far credit bubbles can take you, and there are signs we may finally be getting there.

Big mortgages would rapidly become a lot less popular if prices weren't a one-way bet guaranteed by the government.

Pretty sure it must be percentage of the 1997 value, otherwise it's hard to understand how the scale can accomodate both house prices and population in a single set of units.

{kind=link}